How Mercury Rose to the Top of Startup Banking

How 10 years of building startups shaped founder Immad Akhund's vision for Mecury the company redefining banking for startups and SMBs

The Slow and Steady Path to Product-Market Fit

Immad Akhund had to work for it. It took him nearly ten years as an entrepreneur to see what product-market fit looked like up close, but once he did, he never really let it go anymore.

After a year working as an engineer at Bloomberg, Akhund started his first company, a British version of Yelp. Seven months in, the company didn’t take off and Akhund decided to start another one. This time, he moved to San Francisco, and got accepted into Y Combinator. Although the second company, a developer tool for access management, attracted millions of users, it didn’t have a clear path to monetization. After two years, it was acqui-hired, and Akhund went on to start another project.

His third venture, Heyzap, lasted much longer. The company started as a flash game network for desktop and raised funding from Union Square Ventures, Naval Ravikant and Chris Dixon. After three pivots and 6 years of iterations, it launched a developer tool to let apps connect to and optimize across several ad networks simultaneously. Very quickly, the product took off and the company substantially increased revenue two years in a row. In 2016, the business was doing so well that Akhund sold it to RNTS Media for $45m.

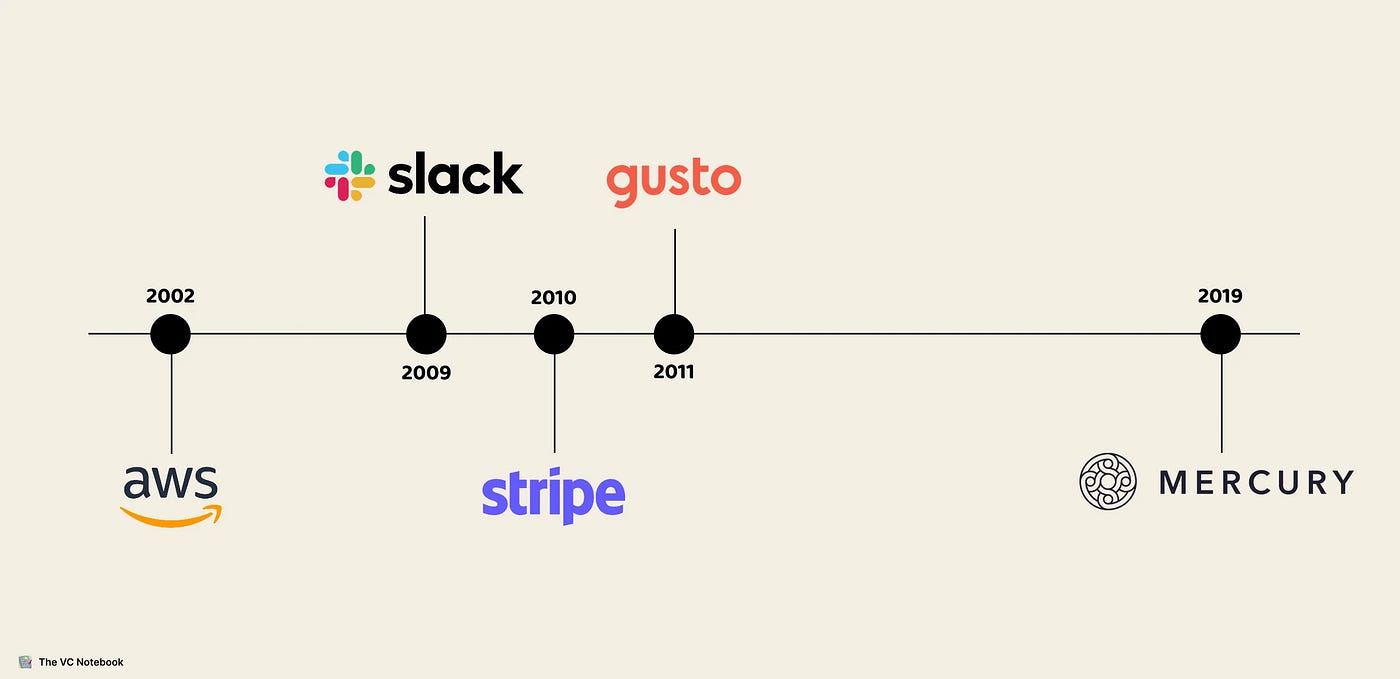

Through this ten year arc as a repeat entrepreneur, Akhund was able to witness firsthand how new, intuitive tools were helping entrepreneurs launch their business (what he calls the consumerization of business software) more easily. When he started his second company, representatives from payroll behemoth ADP showed up to his office with a literal briefcase filled with files for him to fill out and sign. Then Gusto came around and digitized the entire payroll process. At the same time, Stripe and Slack were making online payments and company communications much smoother. To Akhund, a better bank account seemed like an obvious missing piece.

In 2013, he met with founders of a YC startup called TrueLink. The company was working on a secure debit card for seniors and had signed a partnership with a bank to launch their product. This struck a chord with Akhund. Once again, he thought, Silicon Valley showed him the possibilities were far greater than what he could imagine. Seeing these younger founders deal with financial institutions convinced Akhund building a bank account for startups was doable, and he could be the one to do it.

But still fully committed to Heyzap, he shelved the idea, believing someone would tackle the problem. Although a few entrepreneurs gave it shot, none executed it the way he had envisioned. When he sold his business and started thinking about his next move, he considered going into VC. After a few angel investments however, he noticed an unsettling truth. The founders that needed his help wouldn’t listen to his advice, while the best ones would not contact him at all. Akhund recalls investing early in Rappi, the Latin American super-app, and not hearing from its founder until the company had become a unicorn.

So after a year working of working at RNTS, Akhund decided to go back to entrepreneurship and pursue his banking idea, along with two former Heyzap colleagues, Max Tagher and Jason Zhang. “I had a list of ideas to go down. I feel like those were my top three ideas: the bank, the API for a CRM, and a kind of hardware tool for remote work. The bank one had been in my head for years”, Akhund would recall. As no one had really done it right, he decided to give his idea a shot.

After interviewing dozens of founders and draining as much information as he could from fintech lawyers, Akhund was ready to make his move. The timing, Akhund would reflect several years later, was also perfect. Banking-as-a-Service was taking off, opening up infrastructure to startups and making it possible for new products to be built on top of legacy, but trusted foundations, without the need to get a charter. Also, startup funding was ballooning. To start a digital bank, Akhund thought, required a sizeable chunk of seed capital, even without having to fill all the requirements expected to form a full-fledged bank. As part of his discovery, Akhund had riffed frequently with Andreessen Horowitz partner Alex Rampell, who had invested in Cross River Bank. When the time came to raised his Seed, Rampell led the $5m funding round.

To build Mercury, Akhund asked himself a simple question: “What does it take for this to be your only bank account as a business?” Interviewing founders didn’t bring that much insight: when asked if they wanted a better banking product, they couldn’t really imagine the experience being that much better (no matter how terrible it was).

But Akhund had his own conviction to rely on. The product he wanted to release had to fulfil two specific needs: it needed to support international wire transfer, and it had to be able to work for immigrant founders. What’s more, it would allow for online sign-ups (which traditional banks to this day do not provide). Contrary to Silicon Valley conventional wisdom, he also knew he wouldn’t release a half-baked product or an MVP. “I don’t think you can iterate yourself to a new bank”, he would reflect. When imagining an entirely new experience, it can indeed make sense to release a first iteration of a product to see how customers interact with it. With a bank account, there are a set of features that simply need to be there when the product launches for it to be a credible alternative to what’s on the market.

With this clear vision in mind, Akhund tied a partnership with BBVA, which had just recently acquired Simple, a consumer focused neo-bank. A year into building the product, it became clear the bank wouldn’t deliver on its commitments, which prompted Mercury into finding another partner. The last-minute change turned out to be a blessing. The extra six months the company had to work on back-end fixes also gave the team time to polish the user experience and interface. Akhund and his co-founders were able to perfect the onboarding process, which left a lasting impressions on users.

When Mercury was finally ready to launch, in April 2019, it caught fire. “Mercury was product-market fit from the day we launched. We just grew by 30, 40% a month for the first year”, Akhund would recall. Four months later, in September, Mercury was already generating $1m in annualized revenue.

This early growth caught the attention of investors. In September of 2019, CRV Partner Saar Gur led a $20m Series A round at a $100m valuation. Convinced business banking could be disrupted by a product-led approach, the CRV partnership found their ideal candidate in Mercury: “We’d been exploring the opportunity in B2B banking for many months but hadn’t found the perfect fit until we connected with Mercury” Gur wrote in the firm’s Series A announcement. Adding to Akhund’s point on perfect timing, he also noted that targeting startups in the 2017–2019 era was the right time given the increased funding that allowed startups to proliferate and therefore mechanically increase the size of Mercury’s initial target market.

Growing the Core Banking Product

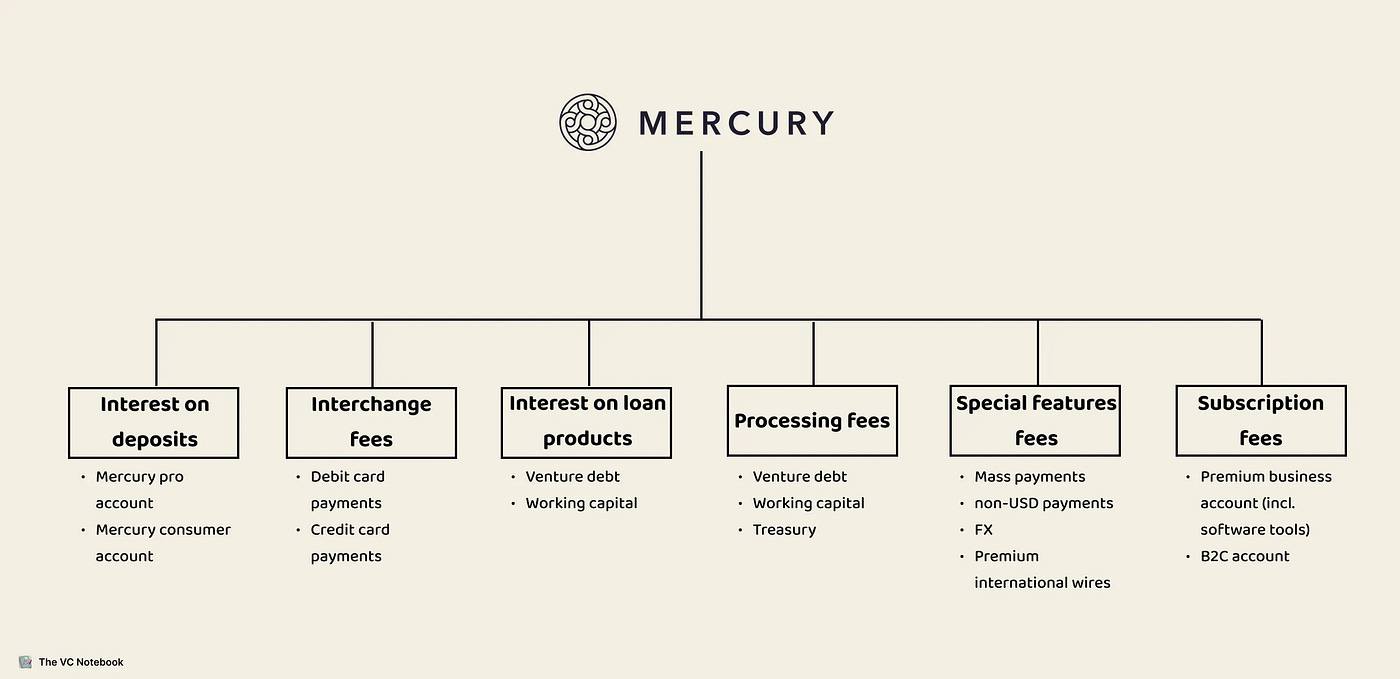

As the world was nearing a total shutdown in March 2020, Mercury’s revenue came from two main sources: interest earned on customer deposits and interchange fees from debit card transactions. With interest rates heading towards zero, 60% of Mercury’s revenue was in jeopardy. The jump-scare lasted only a couple of months however, with the company promptly bouncing back with the spike in e-commerce that resulted from global lockdowns.

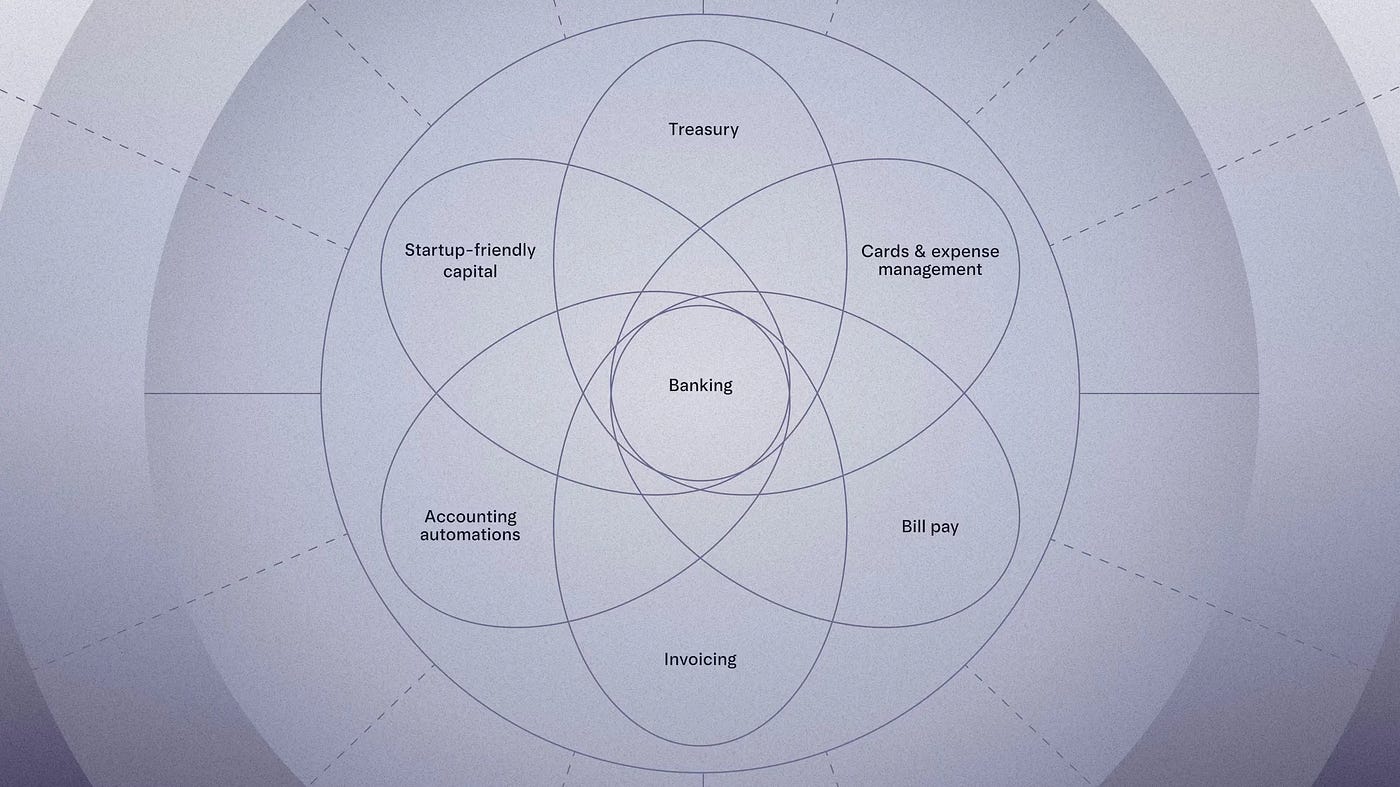

With this model in place, Mercury focused its first year and a half on improving its core product. Akhund knew from the start that banking would stay at the core of his company’s offering, as it is to this day.

By the end of the year 2020, the company released its first product outside core banking: Treasury. The launch embodied Mercury’s product approach moving forward. The company would go on to treat every product launch as an internal startup: start with a very small team to prove the concept, then scale it with additional investment guarded by ambitious KPIs that are monitored quarterly and paced with strict and tight milestone deadlines. The Treasury project, as an example, took a team of 6 engineers and 3 designers 9 months to deliver.

The product, built in partnership with Apex Clearing Corp, allows companies that have cash sitting in the bank to invest it in mutual funds that buy low-risk debt, with Mercury taking a small fee on monthly deposits (between 0.15% and 0.6%). In addition to diversifying the company’s revenue streams, it set the stage for subsequent product releases that would revolve around the bank account and help founders make the most of their finances.

Lower interest rates also ushered in a ZIRP-fueled investing frenzy in 2021, with Fintech being one of its main beneficiaries. Although it stayed cool-headed during the period, Mercury did raise a $120m Series B led by Coatue in July 2021, reaching unicorn status in the process.

Staying true to its mission to become the financial nervous system of its customers, Mercury released two key products in 2022. Its Credit Card IO was a hit and quickly became Mercury’s customers’ credit card of choice. The second product, a Venture Debt Facility, allowed founders to take on non-dilutive financing at attractive interest rates, with favorable payback terms. Jason Garcia, who led the effort, called it “a labor of love”, echoing Mercury’s focus on building compelling products with care and craftsmanship. It also created a new revenue stream for the company, which monetized the product through generation fees and interest collection.

The Sweep Network, Mercury Vault and the SVB Collapse

Getting a bank charter for a startup is almost impossible. Regulators, as Akhund says, want banks to be low-growth, low risk institutions. Startups, by essence, are the exact opposite. To roll out its core banking product, therefore, Mercury tied a partnership with a local bank, Evolve Bank, and a BaaS supplier, Synapse. Mercury would provide its clients with the banking experience, without ever touching their money.

Indeed, deposits would be handled by Evolve, and later Choice financial Group. And although one client deposited $1m in their account one week upon signing up, Mercury still had to assure its clients their hard-earned deposits were safe with the young startup. Thanks to the relationship with Evolve, which operated within a Sweep Network, client deposits were ensured up to $1m.

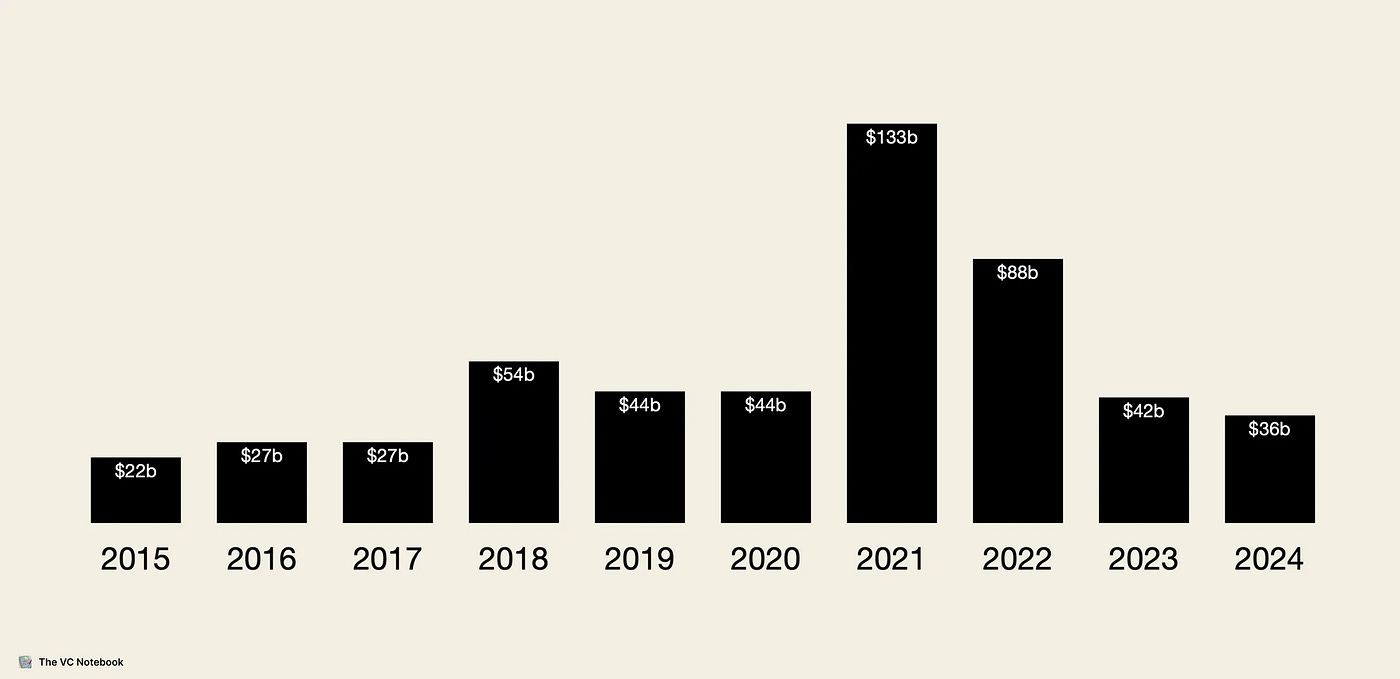

As a result, Mercury headed into 2023 with a strong war chest and a solid suite of banking products targeted at startups. What it couldn’t anticipate was the collapse, in March, of its main competitor, Silicon Valley Bank. The funding frenzy saw the tech ecosystem’s main bank grow its total deposits from $62b in March 2020 to $124b only a year later. When the long-term treasury bonds the bank was holding fell in value due to the rise in interest rates, Founders Fund and other firms urged their startups to take out their deposits, leading to $42b in withdrawals and leaving SVB with a negative cash balance. Given the systemic risk this posed, the Federal Government backstopped the losses.

Nonetheless, deposit insurance took center stage. Mercury seized the moment to develop and launch Mercury Vault over the same week-end the events were unfolding, increasing customer deposit insurance to $5m. The collapse gave the company a strong customer acquisition boost, with 26,000 new customers joining the company in the aftermath of SVB’s collapse (at the time, the company had 100,000 customers).

Expanding into financial software and consumer

Although the company kept growing at breakneck speed in 2023 and 2024, it stayed true to its founding principles. It stayed customer obsessed and focused on delivering products that made its customers’ lives easier. 2024, notably, was its most ambitious product-wise.

Indeed, in May, the company released its financial workflow tools. Once again, product market fit for some of them was immediate. Its invoicing tool for instance, was built because customers were finding workarounds with the Mercury’s Request Payments features to generate invoices. This set of releases further cemented Mercury’s compound approach. As more customers signed on to the Mercury bank account, the company’s scale justified developing more products and features to bolt on to its core.

As a result, Mercury rolled out Bill Pay, Invoicing, Accounting Automation and Employee Reimbursements, further expanding its business model and creating a subscription revenue stream.

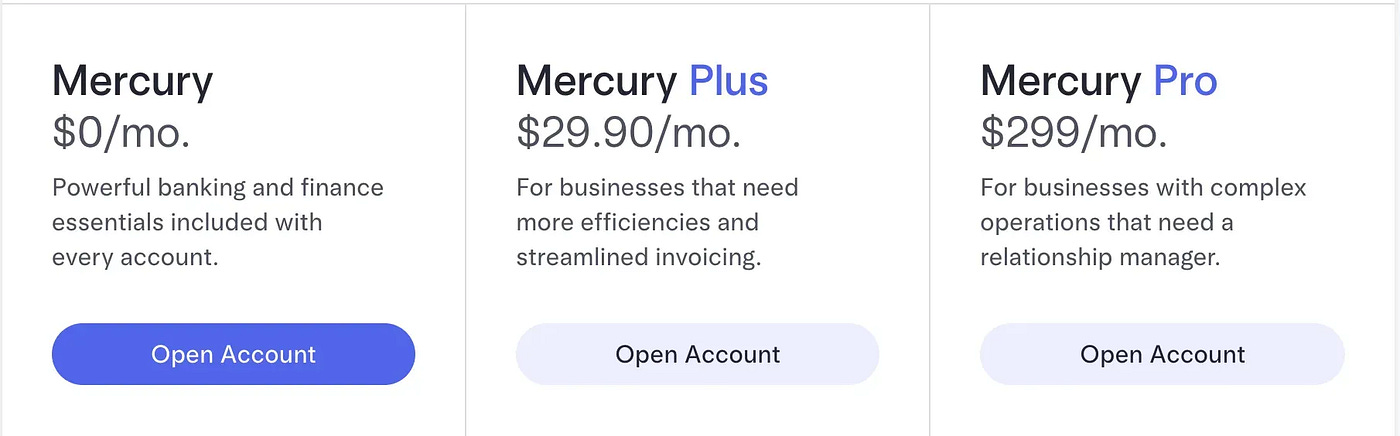

A banking product is often in the hands of a few key people in the startups. Founders, heads of finance and others interact with the product daily. Because of this, the experience offered by Mercury left many wondering: why didn’t the same experience exist for consumer banks? Although consumer apps offered a smoother experience than business banks, Mercury had now set the standard for what a top tier banking experience could be. What’s more, because it targeted startups, its product was used by tech savvy, sometimes wealthy people who would be more than willing to adopt the product for personal use. Feeling the pull, Mercury announced in April 2024 that it would be rolling out its consumer-facing product, priced at an annual $250 fee. With 200k existing business customers, it was not hard to envision this product generating tens of millions in annual revenue.

Becoming the bank

While the company was diversifying its revenue model, it was operating through partnerships with Synapse, Evolve and Choice Financial. That changed when, in October 2023, Mercury and Evolve announced they would respectively cease working with Synapse and collaborate directly. The abrupt end of the partnership cut the BaaS platform from a significant revenue stream, eventually leading to its unravelling and bankruptcy.

A few months later, Mercury announced that it would no longer be working with Evolve either, blaming the bank’s risk management policies. Although Mercury anticipated the end of its partnership with Evolve by onboarding Column NA in October 2024, cracks were starting to show in the partnership model. While beneficial in the beginning to gain trust from customers, as well as handle complex Risk and Compliance workflows, it limited Mercury in its ability to fully control the product experience. For a design-obsessed organization, this meant the model had an expiration date.

Bolstered by their May 2025 $300m Series C, led by Sequoia, at a $3b valuation, the firm decided it was time to stand on its own two feet. Mercury’s brand, its dominance in the startup ecosystem (33% of venture backed startups have Mercury), and strong financials ($500m in Revenue for 2024, profitable in the past three years) were enough arguments to convince Akhund and his team to apply for a bank charter. In December, it announced it had applied for a National Bank Charter, with the objective of delivering “a better customer experience at scale”, while ensuring “greater stability, long-term confidence, and trust.”

The path ahead — compounding, culture and focusing on oneself

9 years after inception, and 7 after launching its product, Mercury has experienced incredible success, and has set itself up perfectly for the future. Its core product, a corporate bank account with online sign up and state-of-the-art UX, has led the company’s growth from day one.

Mercury’s main acquisition channel remains word-of-mouth, with 50% of new customers joining organically, the remaining 50% stemming from both partnerships with the likes of Stripe Atlas or accounting firms, and Google Ads. Its diversified revenue streams encompass interest earned on deposits, interchange fees, loan processing fees and interest earned on loans, fees for specific transactions and subscription fees, both on the B2B and B2C side.

Besides the spotless execution, customer obsession and design-centricity this progress required, it can be argued that Mercury has been so successful in compounding because it has managed to insert itself deeply into the startup ecosystem.

Akhund’s history as a repeat entrepreneur who went through YC twice and invested in over 300 companies has contributed to Mercury cementing its reputation as the go-to bank for startups: “Part of Mercury’s success has been my connection with early stage founders. From the thirty first alpha customers we had, 100% of them I had invested in”, Akhund admits.

Mercury Raise, a discontinued program, worked as a cohort-based program that helped accelerate $1.7b in funding across 635 startups. More recently, Akhund has announced he was launching his own Venture Firm with a first $26m fund.

These initiatives keep the Mercury flywheel turning: the more embedded in the startup ecosystem Mercury finds itself, the larger share of startups it can hope to catch at inception (nearly 40% of new startups open an account with Mercury, depositing over half their cash with the bank, as of 2024). Banking being a highly sticky product, this creates long-lasting customer relationships, with users who can provide valuable and cutting-edge feedback into further improving the product.

Beyond its central position in the startup ecosystem, Mercury has also adopted a long-term approach in building the company. This is most noticeable in its culture, that Akhund and his cofounders have been deliberate in shaping from the start. “The process for culture, Akhund believes, “is you write it down: what do you care about? how do you care about it? That’s step one. Step two is how do you then put a hiring process that tries to pick people who have that cultural attribute. Because you’ve stated what you care about and you hire against it, then you start doing these things that reinforce it.”

Although the company has significantly grown its headcount, from 60 people in 2020 to over 1000 by the end of 2025, it has put an emphasis on hiring curious, humble and detailed-oriented people. As part of the hiring process, candidates have to give a 40-minute presentation on any topic of their liking. This reveals how curious a candidate can be, as “curious people just have this weird level of detailed attention to some random things”, Akhund believes. Focusing on the long term, he has also implemented a contrarian six-year vesting plan for employee stock options, taking a page from Naval Ravikant’s playbook. Ensuring people feel invested in the company and stick around for longer than the Valley’s typical two or three years is really important to Akhund: “I really want people to have a lot of ownership in Mercury”, he claims.

The past years have seen players such as Stripe, Brex or Ramp significantly strengthen their product line-ups with financing and accounting automation products. While Akhund downplays the importance of competition, stating that Brex and Ramp have a slightly more enterprise-focused positioning, they are still playing on the same field.

However, banking is one of the largest sectors globally, with revenues topping $5.5 Trillion in 2024. This leaves more than enough room for several giants to emerge in the sector. Akhund’s experience as an entrepreneur, once again, guides his philosophy on the topic. While he would worry about competitor moves at his previous company, they would never end up proving material to his own trajectory. When he started Mercury, he decided competition wouldn’t be at the center of attention, that he would “just focus on customers, focus on product.” This customer obsession has worked wonders for the company so far. And it seems like the right compass to follow in their endless “pursuit of radically different banking”.